HAPPENING NOW! At Inman Connect Las Vegas, July 30-Aug. 1, 2024, the noise and misinformation will be banished, all your big questions will be answered, and new business opportunities will be revealed. JOIN US VIRTUALLY.

Bond market investors who fund most home loans have cleared mortgage rates to continue their descent from 2024 highs after Fed policymakers dropped hints Wednesday that a September rate cut could be in the cards.

Wrapping up a two-day meeting Wednesday, members of the Federal Open Market Committee (FOMC) said they’d leave their target for the short-term federal funds rate at between 5.25 percent and 5.50 percent, as expected.

TAKE THE INMAN INTEL INDEX SURVEY FOR JULY

But the committee made some subtle changes to the language of its post-meeting statement explaining its rationale, Pantheon Macroeconomics Chief Economist Ian Shepherdson noted in an email to clients.

Ian Shepherdson

“Progress towards the committee’s 2 percent inflation objective has been upgraded to ‘some,’ from ‘modest,’ and inflation now is described as only ‘somewhat’ elevated,” Shepherdson wrote of the changes from June’s statement. “Meanwhile, the risks to achieving the employment and inflation goals ‘continue to move into better balance,’ and the committee now is ‘attentive to the risks to both sides of its dual mandate,’ rather than just to the inflation risks.”

In other words, Fed policymakers are acknowledging that while they’re determined not to cut rates until they’re certain that inflation is tamed, they’re also afraid of waiting too long to ease and throwing the economy into a tailspin.

Data released last week showed the Federal Reserve’s preferred measure of inflation, the personal consumption expenditures (PCE) price index, dropped to 2.51 percent in June from a year ago — just half a percentage above the Fed’s 2 percent target.

Mike Fratantoni

“The FOMC did not change its target for the federal funds rate but did shift its statement to acknowledge that inflation is slowing, unemployment is rising, and that there are now more balanced risks to the economy,” Mortgage Bankers Association Chief Economist Mike Fratantoni said in a statement. “While the Fed still hopes for a slower rate of inflation, there is a greater risk now that keeping monetary policy overly tight for too long could lead to unnecessarily higher unemployment.”

At a press conference following the meeting, Fed Chair Jerome Powell dropped more hints that the central bank will be ready to cut rates if it sees signs the economy is weakening.

“We know that reducing policy restraint too soon or too much could result in a reversal of the progress that we’ve seen” on inflation, Powell said. “At the same time, reducing policy restraint too late or too little could weaken economic activity and employment.”

Powell: ‘We are prepared to respond’

“If the economy remains solid, inflation persists,” Powell warned. “We can maintain the current target range for the federal funds rate as long as appropriate. If the labor market were to weaken unexpectedly or inflation were to fall more quickly than anticipated, we are prepared to respond.”

But the CME FedWatch tool, which tracks futures markets to gauge the odds of future Fed moves, shows investors are not only certain that the central bank will cut rates by at least 25 basis points in September but that there’s an 18 percent chance it will approve a more drastic cut of 50 basis points. A basis point is one-hundredth of a percentage point.

Bets placed by futures market investors as of Wednesday also suggest they see a 75 percent chance the Fed will cut rates by at least 75 basis points by the end of the year, up from 20 percent a month ago.

Shepherdson said forecasters at Pantheon Macroeconomics are only expecting the Fed to cut rates by 25 basis points in September, but that it will follow up with 50 basis-point reductions in both November and December.

That would bring the short-term federal funds rate down 1.25 percentage points, to a target range of 4 to 4.25 percent.

“Our view remains that the Fed is recognizing too slowly that the labor market is cooling and that high inflation is yesterday’s problem,” Shepherdson wrote. “With rates well above neutral, the easing cycle likely will be much faster than markets currently anticipate if, as we expect, the labor market data continue to weaken and inflation prints remain benign.”

Fratantoni said MBA forecasters are holding to their call for two rate cuts totaling 50 basis points this year.

Barometer for mortgage rates falls

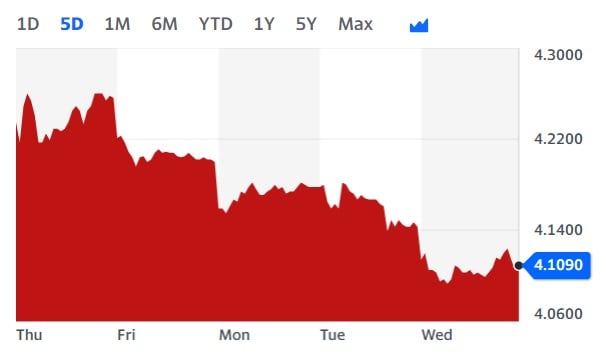

Yields on 10-year Treasury notes flirted with 4 percent Wednesday. Source: Yahoo Finance.

Yields on 10-year Treasury notes, a barometer for mortgage rates, remained on track for another weekly and monthly decline after Powell’s press conference. Since hitting a 2024 high of 4.74 percent on April 25, rising demand for bonds by investors who expect the economy to slow has brought yields on 10-year Treasurys down more than half a percentage point.

After closing at 4.14 percent Tuesday, 10-year Treasury yields touched a low of 4.09 percent Wednesday morning before rebounding to close at 4.11 percent Wednesday. That’s a 38 basis-point drop from July 1 and a 63 basis-point drop from a 2024 high of 4.74 percent on April 25.

Conforming mortgage rates in free fall

Rates for 30-year fixed-rate conforming mortgages averaged 6.71 percent Tuesday, down 30 basis points from July 1, according to rate lock data tracked by Optimal Blue.

Since hitting a 2024 high of 7.27 percent on April 25, rates on conforming mortgages have come down by 56 basis points — more than half a percentage point.

Borrowers seeking jumbo mortgages that exceed Fannie Mae and Freddie Mac’s $766,550 conforming loan limit haven’t seen as much relief, as the “spread” between jumbo and conforming loans has widened.

Borrowers were accepting locks on jumbo loans Tuesday at an average rate of 7.22 percent — a more modest drop of 34 basis points from a 2024 high of 7.56 percent registered on April 15.

Before the pandemic, rates on jumbo mortgages tended to be lower than conforming loans by an average of 9 basis points from 2017-2019, according to Optimal Blue data. But tightening by regional banks, which are major providers of jumbo loans, has flipped the spread, with rates on jumbo mortgages averaging 16 basis points above conforming loans in 2023 and 30 basis points so far this year.

With Fed rate cuts on the horizon, bond market investors who fund most conforming mortgage loans are happy to accept lower yields on mortgage-backed securities (MBS) backed by conforming loans. But jumbo lenders typically hold loans on their books, and their funding costs may come down more slowly.

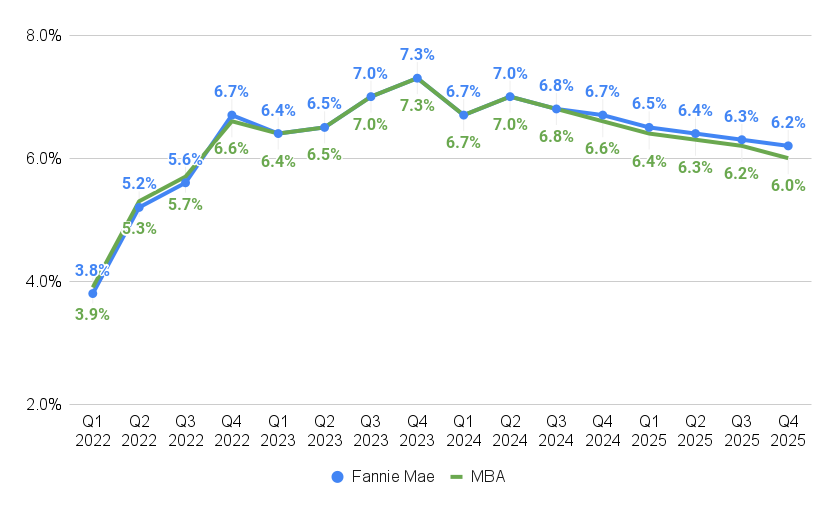

Economists at Fannie Mae and the Mortgage Bankers Association (MBA) predict the rate on conforming loans will continue to drop into the low sixes by the end of next year.

Mortgage rates forecast to drop

Source: Fannie Mae and Mortgage Bankers Association forecasts, July 2024.

“Mortgage rates are now well below 7 percent, and there has been some modest pickup in refinancing activity in recent weeks,” the MBA’s Fratantoni said. “We expect that mortgage rates will continue to drift lower through the remainder of the year, particularly if the Fed does launch a series of rate cuts in September.”

So far, homebuyers have been slow to respond to the decline in rates, as the runup in home prices during the pandemic and elevated rates have priced many would-be buyers out of the market.

A weekly survey of lenders by the MBA showed applications for purchase loans were down by a seasonally adjusted 2 percent last week compared to the week before and were 14 percent lower than a year ago. Applications to refinance were down 7 percent week over week, but up 32 percent from a year ago.

Eric Orenstein

“Even with a September rate cut possible, mortgage companies will continue to face meaningful earnings headwinds for the foreseeable future,” Fitch Ratings Senior Director Eric Orenstein said, in a statement. “With most outstanding mortgages still carrying rates below 5 percent and record home prices driving down affordability, it may be a long road back to higher origination volumes.”

Get Inman’s Mortgage Brief Newsletter delivered right to your inbox. A weekly roundup of all the biggest news in the world of mortgages and closings delivered every Wednesday. Click here to subscribe.